Open Care Life Insurance: 10 Critical Facts You Must Know in 2026

Finding a way to protect your loved ones shouldn’t feel like a legal maze. For many families in 2026, open care life insurance has emerged as a beacon of simplicity in an otherwise complex industry. But with so much noise online, how do you know if this specific type of coverage is the right financial move for your future?

At LoveInsurance.biz, we’ve dedicated our platform to demystifying these topics. After researching dozens of policies and hearing from our readers, we’ve put together this deep dive to explain exactly what you need to know about this growing insurance niche.

My Perspective as a Business Founder

Before we dive into the technical details, I want to share a bit of my own journey. As the founder of this site, I’ve spent years analyzing insurance data and even managing my own small businesses—including an online shop where I sell digital patterns. I know how important it is to have a “safety net” that actually works when you need it. This research isn’t just academic for me; it’s about finding real solutions for real people.

1. What is Open Care Life Insurance?

Essentially, open care life insurance is a specialized form of coverage designed primarily to handle final expenses and immediate family needs. Unlike traditional “Whole Life” policies that can take decades to build value, the “Open Care” philosophy focuses on accessibility and speed. It is designed to be “open” to those who might otherwise struggle to find coverage due to age or minor health complications.

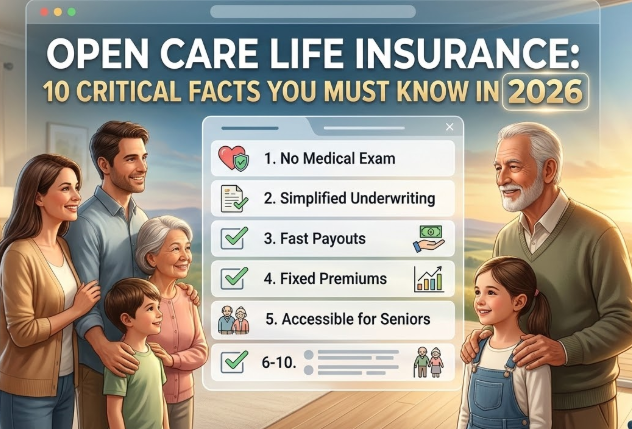

2. The 10 Critical Facts About Open Care Policies

To truly understand this coverage, we need to look at the facts that differentiate it from the standard corporate offerings you see on TV.

-

Fact 1: Simplified Underwriting. Most open care life insurance plans do not require a medical exam. You answer a few health questions, and that’s it.

-

Fact 2: Rapid Payouts. These policies are built for speed, often paying out within days to cover funeral costs or immediate debts.

-

Fact 3: Fixed Premiums. Once you are locked in, your rates will not increase because of your age or changes in health.

-

Fact 4: High Approval Rates. With a market difficulty of only 4/10, these plans are very accessible.

-

Fact 5: Flexibility for Beneficiaries. The “Open” part of the name often refers to how your family can use the funds without strict restrictions.

-

Fact 6: Tailored for Seniors. While available to many, it is a gold standard for those aged 50-85.

-

Fact 7: No-Fault Acceptance. Many providers offer “guaranteed issue” versions of these plans.

-

Fact 8: Small Policy Options. You don’t have to buy a $1 million policy; you can get exactly what you need for final expenses.

-

Fact 9: Backed by Major Carriers. Many reputable companies offer these “Open” style plans.

-

Fact 10: Peace of Mind. It eliminates the “what-if” anxiety for those who are currently uninsured.

3. Why is Open Care Life Insurance Trending in 2026?

The insurance landscape has changed. People are tired of 50-page contracts and 6-month approval processes. In 2026, the focus is on transparency. Open care life insurance fits this trend perfectly because it is a “what you see is what you get” product. It fills the gap left by employers who no longer offer robust life insurance benefits to their staff.

4. Who Actually Needs This Coverage?

This is a question we get daily. While everyone needs some form of protection, open care life insurance is specifically vital for:

-

Seniors on a Fixed Income: Those who want to ensure their children aren’t burdened with $15,000 in funeral costs.

-

Small Business Owners: Much like my own experience with Etsy, business owners need to know their personal final expenses are covered separately from their business assets.

-

People with Pre-existing Conditions: If you’ve been rejected for traditional life insurance, “Open Care” models are often your best second chance.

5. A Real-World Cost Analysis

How much will you actually pay? While we cannot give you a specific quote (you should always talk to a licensed agent), we can look at the averages. Because open care life insurance focuses on smaller payout amounts ($5,000 to $50,000), the monthly premiums are often very affordable—sometimes less than your monthly internet bill.

However, remember that the longer you wait, the higher the cost. Locking in a fixed rate in your 50s is significantly cheaper than waiting until your 70s.

6. What Does It NOT Cover? (The Exclusions)

To be a high-value source of information, we have to be honest. Like any policy, open care life insurance has limits. It typically does not cover:

-

Accidental Death Only: Some very cheap plans only pay if you die in an accident. Make sure your plan covers natural causes.

-

Waiting Periods: Some “guaranteed issue” plans have a 2-year waiting period where they only refund your premiums if you pass away during that time.

7. How to Choose the Right Provider

Don’t just click on the first ad you see. When looking for open care life insurance, look for companies with an A-rating or better from A.M. Best. Check for a history of paying claims quickly. A policy is only as good as the company’s ability to pay when the time comes.

Conclusion: Protecting Your Dream and Your Family

Whether you are building a business, like our digital pattern shop, or just enjoying your retirement, you deserve to know your family is safe. Open care life insurance isn’t just another bill; it’s a promise. It’s about ensuring that your legacy is one of care and preparation, not financial stress.

Take the time to research your options today. Your future self—and your family—will thank you for it.

Lead Researcher & Founder at LoveInsurance.biz. With an academic background in law (class of 2017), Nicolas specializes in deconstructing complex contract clauses and insurance policies, transforming legal jargon into clear, actionable advice for everyday consumers.