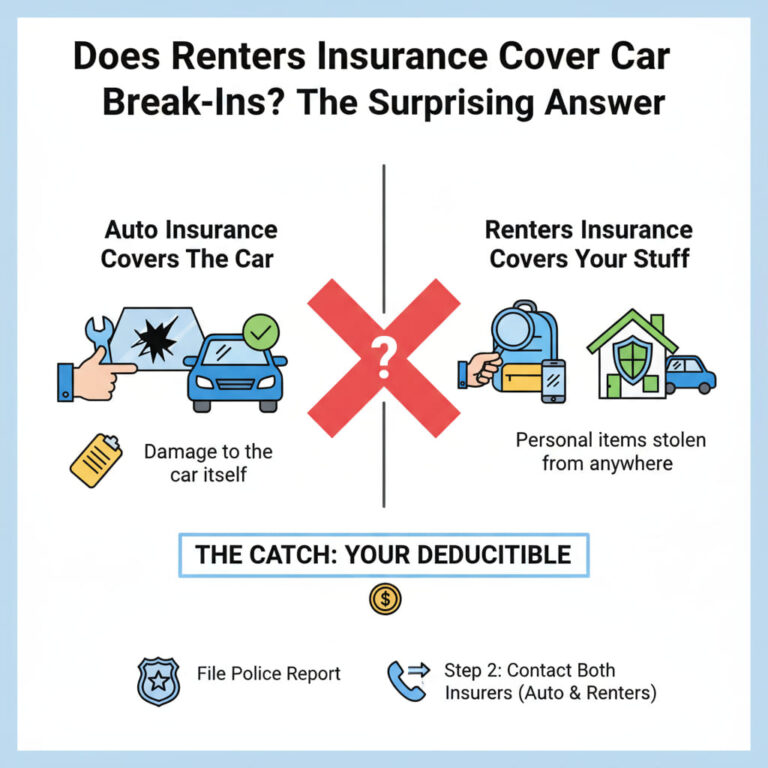

Does Renters Insurance Cover a Stolen Laptop From a Car? (3 Rules)

For modern professionals and freelancers, a laptop is much more than just a piece of electronics. It is your office, your creative studio, and your livelihood. Leaving it hidden under a car seat while you run into a coffee shop seems harmless—until you return to a smashed window and a missing backpack. This leads to an urgent question: does renters insurance cover a stolen laptop from a car? The short answer is a resounding yes. Let’s break down exactly how this coverage works.

How Does Renters Insurance Cover a Stolen Laptop From a Car? Many people mistakenly believe that renters policies only protect items physically located inside their apartment. In reality, a standard policy includes “off-premises” personal property coverage.

According to the Insurance Information Institute, your belongings are protected essentially anywhere in the world. Whether your laptop is swiped from a table at a local cafe or snatched from the backseat of your parked vehicle, your renters insurance steps in to cover the loss.

(Note: While your policy covers the stolen item, it will not cover the broken car window. For a comprehensive breakdown of the vehicle damage itself, check out our master guide: Does renters insurance cover car break ins).

The Two Hurdles: Deductibles and Depreciation Before you celebrate, you need to understand two critical factors that determine your actual payout:

1. Your Insurance Deductible Your deductible is the amount you must pay out-of-pocket before the insurance company pays a dime. If your stolen laptop was worth $1,200 and your deductible is $500, the insurance company will only cut you a check for $700.

2. ACV vs. Replacement Cost How is your laptop valued?

-

Actual Cash Value (ACV): The insurer pays what the laptop was worth at the time it was stolen, factoring in depreciation.

-

Replacement Cost Value (RCV): An RCV policy will pay out enough money for you to buy a brand-new laptop of the same make and model at today’s retail prices.

Watch Out for “Electronics Sub-Limits” Insurance companies are well aware of how expensive modern technology is. Because of this, most policies have “sub-limits” (a maximum payout cap) for specific categories of high-value items, including electronics.

Your overall personal property limit might be $30,000, but your policy might strictly cap electronic payouts at $1,500 per claim. If you had a custom $3,500 video editing laptop stolen, standard coverage won’t be enough. You will need to ask your agent about adding an “endorsement” or “scheduled property rider” to fully insure the item’s appraised value.

Does Your Laptop Belong to Your Business? Here is a crucial detail that often trips up digital business owners: standard renters insurance is for personal property.

If your laptop is exclusively used for your incorporated e-commerce business, or if it was provided to you by your employer, your personal insurance might deny the claim. In those cases, the laptop needs to be covered by a commercial property policy or your employer’s corporate insurance.

3 Steps to File a Laptop Theft Claim If you fall victim to a car break-in, move quickly to secure your claim:

-

File a Police Report: Call the non-emergency police line immediately. You will need a police report number to process a theft claim.

-

Gather Proof of Ownership: Dig up the original receipt or photos of the laptop. Provide the serial number (found in your Apple iCloud or Microsoft Account).

-

Contact Your Insurer: File the claim through your provider’s app. Provide the police report and photos of the forced entry into your vehicle.

Conclusion : Does Renters Insurance Cover a Stolen Laptop From a Car

A smashed car window is bad enough without losing your primary work tool. Fortunately, your policy is designed to be your safety net. So, if anyone ever asks you, does renters insurance cover a stolen laptop from a car, you now know that as long as you understand your deductibles and sub-limits, your digital life is fully protected.

Lead Researcher & Founder at LoveInsurance.biz. With an academic background in law (class of 2017), Nicolas specializes in deconstructing complex contract clauses and insurance policies, transforming legal jargon into clear, actionable advice for everyday consumers.