Collision Deductible Waiver: When Do You Really Need It?

A collision deductible waiver (CDW) is only worth adding to your policy if you live in a state with a high percentage of uninsured drivers and your standard collision deductible is large enough ($1,000 or more) to cause you immediate financial strain. If you drive an older car with a low deductible, or if your state already mandates Uninsured Motorist Property Damage (UMPD) coverage, paying extra for this waiver is likely a waste of money. Here is the direct breakdown of how it works and when you actually need it.

What is a Collision Deductible Waiver?

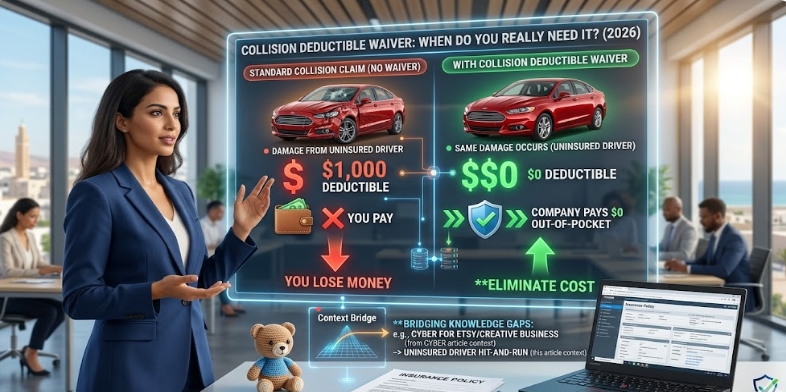

Under normal circumstances, if your car is damaged in an accident, you must pay your collision deductible (e.g., $500 or $1,000) out of your own pocket before your insurance company pays the rest of the repair bill. If the other driver is at fault, your insurance company will try to recover that deductible from the at-fault driver’s insurance and refund you later.

However, if the at-fault driver has no insurance, or it is a hit-and-run, you might never get your deductible back.

A collision deductible waiver is an optional add-on to your auto insurance policy. If you are hit by an uninsured driver, this waiver legally forces your insurance company to pay for the entire repair bill from dollar one. You pay $0 out of pocket.

3 Scenarios Where You Absolutely Need It

1. You Live in a High-Risk State

According to data from the Insurance Research Council (IRC), in states like Florida, Mississippi, and New Mexico, nearly 1 in 4 drivers on the road are illegally driving without insurance. If you live in a state with high uninsured motorist rates, adding a CDW is highly recommended to protect your wallet.

2. You Have a High Deductible to Lower Premiums

Many drivers intentionally choose a high collision deductible (like $1,500 or $2,000) to keep their monthly premiums affordable. If paying that $2,000 out of pocket after an accident that wasn’t your fault would drain your emergency fund, a waiver acts as a vital financial safety net.

3. You Drive a Brand-New or Financed Car

If your vehicle is financed or leased, your lender requires you to carry full coverage. If a hit-and-run driver totals your new car, the last thing you want is to be stuck paying a massive deductible on a car you can no longer drive.

When is it a Waste of Money?

You should skip the collision deductible waiver if:

-

You have a low deductible: If your standard deductible is only $250, the math does not make sense. The extra monthly cost of the waiver over a few years will quickly exceed the $250 you are trying to protect.

-

You have UMPD: In some states, Uninsured Motorist Property Damage (UMPD) coverage essentially does the exact same thing as a CDW. Check your policy declarations page; there is no need to pay for overlapping coverage.

-

You drive a “beater” car: If your vehicle is older and you have dropped collision coverage entirely, you cannot add a collision waiver. It only applies if you carry active collision coverage.

The Verdict

Insurance is about transferring risk. If the upfront cost of your deductible terrifies you, add the waiver. If you have a healthy emergency fund, skip it and save on your monthly premium. Because auto insurance laws vary drastically by state, your best move is to have an independent insurance broker review your policy to ensure you are not double-paying for coverage you already have built-in.

Frequently Asked Questions (FAQ)

Does a collision deductible waiver cover hit-and-run accidents?

Yes, in most states, a hit-and-run is legally classified as an accident with an uninsured motorist. If you have a CDW and file a police report proving it was a hit-and-run, your deductible will typically be waived.

Will my premium go up if I use the waiver?

Generally, no. Because the accident was explicitly caused by an uninsured driver (meaning you are 0% at fault), utilizing your waiver should not trigger a rate increase at your next renewal, though some state regulations vary.

Can I buy a CDW if I only have liability insurance?

No. A collision deductible waiver is an endorsement (an add-on) to a standard collision policy. If you only carry state-minimum liability insurance, you do not have a deductible to waive.

Lead Researcher & Founder at LoveInsurance.biz. With an academic background in law (class of 2017), Nicolas specializes in deconstructing complex contract clauses and insurance policies, transforming legal jargon into clear, actionable advice for everyday consumers.