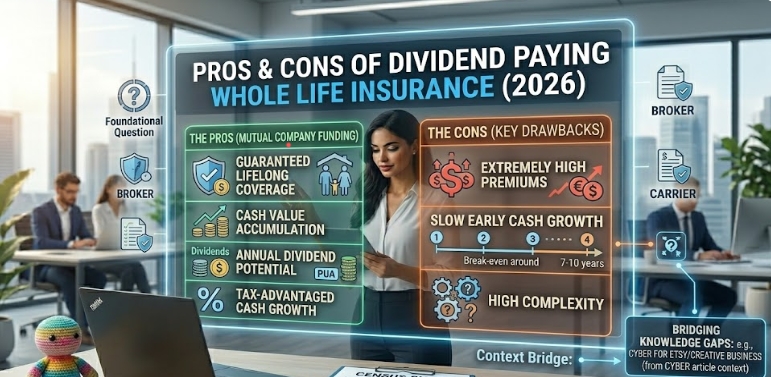

Pros & Cons of Dividend Paying Whole Life Insurance

The short answer is: yes, it is an incredibly powerful financial asset, but it is not for everyone. Dividend paying whole life insurance offers guaranteed lifelong coverage while building a tax-advantaged cash value, but it requires a strict, long-term commitment to high monthly premiums. If you are looking for cheap, temporary coverage, you should buy term life. However, if you want an insurance policy that acts as a conservative, lifelong financial vehicle, here is the direct breakdown of its pros and cons.

What is Dividend Paying Whole Life Insurance?

In the insurance world, this is often referred to as a “participating” policy. When you buy this specific type of whole life insurance from a mutual insurance company (a company owned by its policyholders, rather than Wall Street investors), you are eligible to receive a portion of the company’s annual profits. These profits are distributed to you in the form of annual dividends.

The Pros: Why High Earners Love It

1. Guaranteed Lifelong Protection

Unlike term insurance, which expires after 10, 20, or 30 years, a whole life policy covers you until the day you die, as long as you pay the premiums. The death benefit is guaranteed and will eventually be paid out tax-free to your beneficiaries.

2. Cash Value Accumulation

A portion of every premium you pay goes into a “cash value” account within the policy. This money grows at a guaranteed minimum interest rate on a tax-deferred basis. You can borrow against this cash value to fund a business, pay for a child’s college tuition, or supplement your retirement income without undergoing a credit check.

3. Annual Dividends Add Exponential Growth

The defining feature of dividend paying whole life insurance is the dividend itself. While not legally guaranteed, top-tier mutual companies have paid dividends every single year for over a century. You can take this dividend as cash, use it to lower your premium payments, or—most effectively—use it to buy “Paid-Up Additions” (PUAs), which permanently increases both your death benefit and your compounding cash value.

The Cons: The Hidden Drawbacks

1. Extremely High Premiums

This is the biggest hurdle. A whole life policy can easily cost 5 to 15 times more than a term life policy with the exact same death benefit. If you lose your job or experience a business downturn and cannot afford the high premiums, your policy could lapse, causing you to lose the coverage you paid heavily into.

2. Slow Early Cash Growth

Do not expect to see a massive return on investment in the first few years. Because a large portion of your early premiums goes toward paying the insurance agent’s commission and administrative fees, it typically takes 7 to 10 years for your cash value to equal the total amount of premiums you have paid in.

3. High Complexity

These contracts are notoriously complex. Structuring a policy correctly to maximize cash value and minimize agent commissions requires deep expertise. You should never buy this product online without consulting an experienced, independent insurance broker who can tailor the contract to your specific financial goals.

The Verdict

Dividend paying whole life insurance is best suited for high-income earners, business owners, or individuals who have already maxed out their traditional retirement accounts (like a 401k or IRA) and are looking for a secure, tax-advantaged place to store cash. According to financial experts at Investopedia, choosing a strong mutual company is critical to ensuring your policy performs as expected.

Frequently Asked Questions (FAQ)

Are whole life insurance dividends taxable?

Generally, no. The IRS considers insurance dividends as a “return of premium” (meaning they are giving you back a portion of the money you overpaid). Therefore, dividends are usually not taxed unless the total dividends you receive exceed the total amount of premiums you have paid into the policy.

Can I withdraw my dividends as cash?

Yes. You have several “dividend options” when setting up your policy. You can choose to receive a physical check every year, leave the dividends to accumulate at interest, use them to reduce your next premium bill, or use them to purchase paid-up additional insurance.

What happens to the cash value when I die?

This is a common misconception. When you pass away, the insurance company pays out the total Death Benefit to your beneficiaries. The insurance company generally keeps the accumulated cash value. This is why many financial advisors recommend using or borrowing against the cash value while you are still alive.

Lead Researcher & Founder at LoveInsurance.biz. With an academic background in law (class of 2017), Nicolas specializes in deconstructing complex contract clauses and insurance policies, transforming legal jargon into clear, actionable advice for everyday consumers.